Tax collection in short-term rentals (STR) is the process by which hosts gather and remit government-mandated levies on rental income, occupancy, and sales, directly funding the public services that make tourism markets viable. The role of tax collection in STR goes far beyond a simple line item on a booking summary. Hosts on platforms like Airbnb and VRBO function as de facto tax collectors, responsible for income tax, transient occupancy tax, lodging tax, and local sales tax across multiple jurisdictions. Understanding these obligations is not optional. Non-compliance carries fines, permit revocation, and delisting. This guide breaks down every tax category, clarifies where platform automation ends, and gives you a clear path to full compliance.

What are the main types of taxes STR hosts must understand?

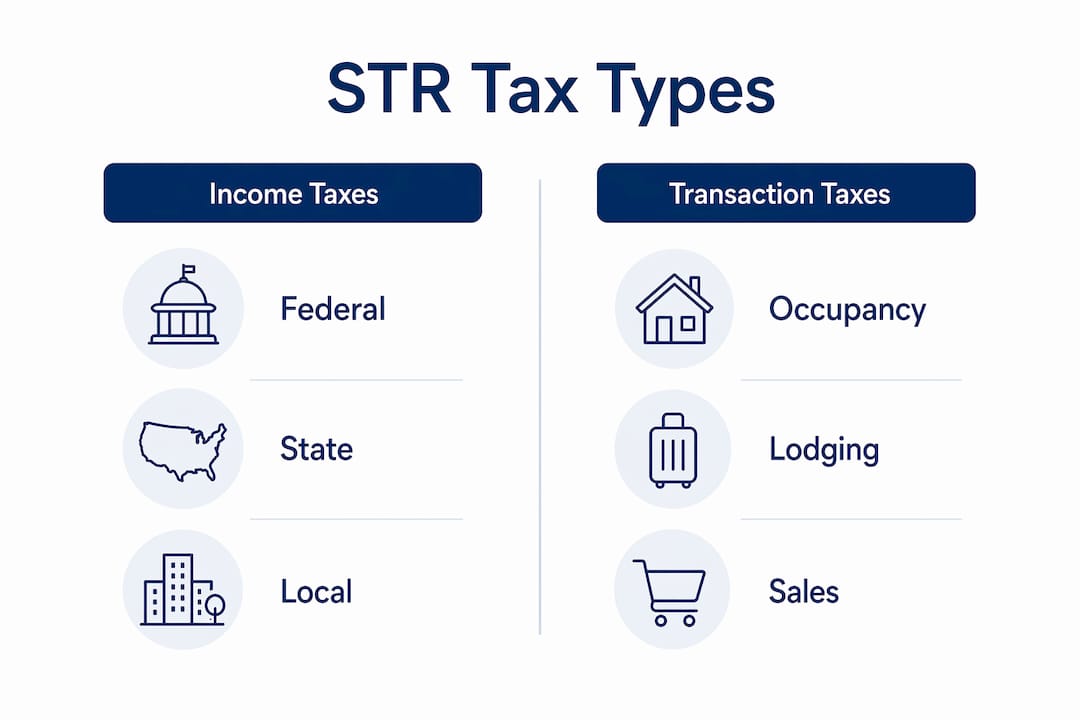

STR hosts face tax obligations at three distinct levels: federal, state, and local. Each level operates on different rules, different tax bases, and different filing requirements.

Federal income tax and the 14-day rule

The federal 14-day exemption rule is the most misunderstood provision in STR taxation. Under this rule, rental income is tax-exempt at the federal level if you rent your property for 14 or fewer days per year. Most active STR hosts rent far beyond 14 days, so federal income tax applies to net rental profits in virtually all practical cases. You deduct allowable expenses such as mortgage interest, repairs, and depreciation from gross rental income to arrive at net taxable income.

State income tax on rental profits

State income tax applies to net rental profits in most states, mirroring the federal structure. The tax rate and filing requirements vary by state, so hosts operating across multiple markets must file in each state where they earn rental income.

Occupancy, lodging, and sales taxes

These taxes operate on gross receipts, not net income. That distinction matters enormously for cash flow planning. Occupancy and lodging taxes typically range from 1% to 20% of gross receipts at the state and local level. A $200 nightly rate in a jurisdiction with a 6% hotel occupancy tax produces a $12 tax charge, bringing the guest’s total to $212. Texas law formalizes this structure, requiring hosts to itemize the tax as a separate line item on every invoice.

The table below summarizes the key tax types, their tax base, and who typically collects them.

| Tax type | Tax base | Primary collector |

|---|---|---|

| Federal income tax | Net rental profit | Host (via IRS filing) |

| State income tax | Net rental profit | Host (via state filing) |

| Transient occupancy tax | Gross receipts | Host or platform |

| State sales tax | Gross receipts | Platform (partial) or host |

| Local lodging tax | Gross receipts | Host (usually) |

One critical nuance: the 14-day federal exemption does not apply to state and local sales or lodging taxes. Colorado hosts, for example, must obtain a sales tax license and remit state and local taxes even for rentals under 14 days. The federal rule is narrowly scoped. Never assume it eliminates your state or local obligations.

You also need the right licenses before collecting any tax. Most jurisdictions require a business license, a short-term rental permit, and a separate sales or occupancy tax registration. Operating without these exposes you to back taxes, penalties, and permit denial.

How do STR platforms facilitate tax collection?

Platforms automate a portion of tax collection, but that automation has firm limits. Understanding exactly where it stops is the most practical thing you can do for your compliance posture.

What platforms actually cover

Major booking platforms collect and remit state-level taxes in many jurisdictions through marketplace facilitator laws. These laws designate the platform as the responsible party for state sales and occupancy taxes on platform-mediated bookings. That covers a meaningful share of your tax exposure, but platform coverage leaves gaps at the county, city, and special district levels. Those local taxes require manual reconciliation and remittance by the host.

Where host responsibility begins

- Local and county taxes: Platforms rarely collect city or county lodging taxes. You must register with each local authority and remit independently.

- Special district taxes: Tourism improvement districts and convention center taxes are almost never covered by platform automation.

- Direct bookings: Direct bookings place 100% tax compliance responsibility on you. You must acquire a tax license, collect the tax from the guest, file returns, and remit funds independently of any platform.

- Multi-platform operations: If you list on multiple platforms, each platform may remit taxes differently. You must reconcile all remittances against your total gross receipts.

Pro Tip: Open a dedicated bank account exclusively for tax funds collected from guests. Never commingle tax receipts with operating income. When a filing deadline arrives, the funds are already set aside and your cash flow remains predictable.

Relying solely on platform-generated tax reports is a compliance risk. Municipal audits consistently find hosts delinquent because they assumed platform summaries covered all obligations. Active personal record-keeping and jurisdiction-specific registration are not optional extras. They are the baseline.

What practical steps should STR hosts take to ensure compliance?

Tax compliance requires a repeatable process, not a one-time setup. The following steps build a system that holds up under audit.

-

Register with every relevant tax authority. Identify all jurisdictions where your property generates income: state, county, city, and any special districts. Register for a sales tax license and an occupancy tax account in each. Do this before your first booking, not after.

-

Reconcile platform remittances against local requirements. Download your platform tax summary each month. Compare what the platform remitted against what each local jurisdiction requires. The difference is your responsibility to collect and pay.

-

Itemize taxes on every invoice. For direct bookings, list each tax as a separate line item. A nightly rate of $200 with a 6% state hotel occupancy tax reads as: Nightly Rate $200, State Hotel Tax $12, Total $212. This practice satisfies Texas Hotel Occupancy Tax requirements and protects you in an audit.

-

Maintain segregated accounts for tax funds. Treat collected taxes as funds held in trust. They belong to the government, not to your business. A separate account prevents accidental spending and simplifies reconciliation.

-

Track filing frequencies by jurisdiction. Some jurisdictions require monthly filing. Others require quarterly or annual returns. Missing a filing deadline triggers penalties even if you owe no additional tax. Set calendar reminders for every jurisdiction.

-

Keep detailed records for at least four years. Retain booking records, platform statements, tax returns, and payment confirmations. Many jurisdictions have a three-year audit window. Four years of records provides a safe buffer.

-

Respond to audit notices immediately. Failure to report or remit accurately can lead to permit revocation or legal action. If you receive an audit notice, gather your records and respond within the stated deadline. Ignoring notices accelerates enforcement.

Pro Tip: Use a spreadsheet or compliance platform to track each jurisdiction’s tax rate, filing frequency, and registration number in one place. When rates change, update the sheet immediately. A single outdated rate applied across hundreds of bookings creates a significant liability.

What broader impacts does effective tax collection have on STR markets?

Tax collection is not just a regulatory burden. It is the mechanism that funds the infrastructure making STR markets viable in the first place.

Local governments use tax revenue from STRs to fund roads, public safety, tourism promotion, and visitor services. These are the exact services that attract guests to a market. A host who collects and remits taxes accurately contributes to the conditions that sustain demand for their own property. The relationship is direct and practical.

“Tax compliance is not just a burden but a crucial participation by hosts in funding the tourism economy and infrastructure that enable their business to thrive. Fair and transparent taxes underpin the legitimacy and sustainability of the short-term rental sector within communities.”

When hosts fail to remit taxes at scale, municipal budgets absorb the shortfall. That shortfall often triggers stricter STR regulations, permit caps, or outright bans. Cities that have experienced widespread non-compliance have responded with aggressive enforcement programs, including third-party tracking and legal action against delinquent operators. The enforcement environment is tightening, not loosening.

Effective tax collection also gives the STR industry political legitimacy. When hosts pay their share, local governments have less incentive to restrict the industry. Transparent, consistent tax remittance positions STR operators as responsible participants in the local economy rather than actors evading their obligations. That distinction matters when city councils debate permit limits or zoning restrictions.

Tax compliance is an active responsibility, not a passive one

Working with STR hosts over the years has shown me one pattern that repeats without fail: the hosts who face audits are almost never the ones who tried to cheat. They are the ones who assumed the platform handled everything.

Platform automation is genuinely useful. It covers a real portion of state-level tax obligations in many markets. But it was never designed to replace host registration, local tax remittance, or direct booking compliance. Treating a platform tax summary as a complete compliance record is the single most common and costly mistake I see.

The hosts who stay out of trouble treat tax management the way they treat property maintenance. They schedule it, they document it, and they do not wait for a problem to appear before paying attention. A dedicated compliance approach that tracks every jurisdiction, every rate, and every filing deadline is not excessive. It is the minimum viable standard for operating legally in multiple markets.

The broader point is this: the STR industry’s long-term viability depends on hosts taking tax obligations seriously. Markets where hosts comply consistently tend to have more stable regulatory environments. Markets where non-compliance is widespread attract enforcement crackdowns that hurt every operator, compliant or not. Your tax remittance is not just about your own risk. It shapes the regulatory climate for the entire market you operate in.

— Jure

How Strcomply helps hosts manage tax compliance

Tax obligations across multiple jurisdictions are genuinely complex. Strcomply is built specifically to reduce that complexity for STR hosts and property managers operating across the United States.

Strcomply’s free compliance check gives you an instant summary of permit requirements, tax obligations by city, and operational restrictions for any listing. Paid plans add a portfolio dashboard with permit tracking, renewal alerts, and regulatory updates so you never miss a filing deadline or a rate change. For hosts managing multiple properties across different markets, Strcomply consolidates the compliance picture in one place, reducing the research burden and the risk of overlooked local requirements. Visit Strcomply to check your listing’s compliance status today.

FAQ

What is the role of tax collection in STR operations?

Tax collection in STR operations requires hosts to gather and remit income taxes, occupancy taxes, and sales taxes to federal, state, and local authorities. Hosts function as tax collectors and are legally responsible for accurate remittance regardless of platform automation.

Does the 14-day rule eliminate all STR tax obligations?

The federal 14-day exemption removes federal income tax liability for rentals of 14 or fewer days per year, but state and local sales and occupancy taxes still apply. Colorado and most other states require registration and remittance even for short rental periods.

What taxes do platforms like Airbnb collect on my behalf?

Platforms typically collect and remit state-level sales and occupancy taxes in jurisdictions covered by marketplace facilitator laws. County, city, and special district taxes are usually not covered, and direct bookings carry no platform tax support at all.

How should I handle taxes on direct bookings?

Direct bookings require you to register for a tax license, collect the applicable taxes from the guest, itemize them on the invoice, and remit them directly to each relevant tax authority. No platform intermediary handles any part of this process.

What happens if I fail to remit STR taxes accurately?

Failure to report or remit accurately can result in permit revocation, back tax assessments, penalties, and legal action. Many jurisdictions now use third-party data analytics to identify delinquent STR operators, making non-compliance increasingly difficult to avoid.

Key takeaways

Effective tax compliance in STR requires hosts to register independently, reconcile platform remittances against local requirements, and manage direct booking taxes without any platform support.

| Point | Details |

|---|---|

| Multiple tax layers apply | Federal, state, and local taxes each have separate rules, rates, and filing requirements. |

| Platform automation has limits | Platforms cover state-level taxes in some markets but rarely handle county, city, or special district taxes. |

| Direct bookings are fully your responsibility | You must register, collect, file, and remit all taxes on direct bookings without platform assistance. |

| Segregated accounts prevent errors | Holding tax funds in a separate account protects cash flow and simplifies audit defense. |

| Non-compliance triggers enforcement | Jurisdictions use third-party tracking to identify delinquent hosts, with consequences including permit revocation. |

Recommended

Check your city's STR regulations

Free compliance reports for 100+ US cities. Permits, taxes, zoning — all in one place.

Check My Address — Free