Many short-term rental hosts assume that listing on a platform means the tax side is fully handled. That assumption is what leads to unexpected fines, back tax bills, and compliance gaps. Understanding what is occupancy tax, and knowing exactly who is responsible for collecting it, is one of the most important legal obligations you face as a host. The rules differ significantly between states, cities, and even counties, and the consequences of getting it wrong are real.

Table of Contents

- What is occupancy tax and who must collect it?

- State and local variations in occupancy tax rates and rules

- Understanding occupancy tax versus sales and other taxes

- Occupancy tax collection and reporting with third-party platforms

- Licensing, registration, and practical compliance steps for hosts

- Why occupancy tax compliance is more complex than most hosts realize

- Simplify occupancy tax compliance with STR Comply

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Occupancy tax basics | Occupancy tax is a state or local tax on short-term lodging rentals, required to be collected from guests by hosts or operators. |

| Varies by location | Tax rates, definitions of taxable stays, and filing requirements differ widely across states and municipalities. |

| Multiple tax types | Hosts must differentiate occupancy tax from sales or use tax, as both can apply separately to short-term rentals. |

| Third-party complexities | Even if platforms collect occupancy tax, hosts often must file returns and reconcile reported taxes themselves. |

| Registration required | Compliance usually mandates registering with taxing authorities and obtaining necessary licenses for short-term rental operations. |

What is occupancy tax and who must collect it?

Occupancy tax is imposed by state or local governments on lodging rentals, and operators must collect it from guests. Put simply, it is a tax on the privilege of renting out a space for short-term lodging. Guests pay it as part of their booking, and you as the host are legally responsible for collecting and remitting it to the correct authority.

The occupancy tax definition covers several names depending on the jurisdiction. You may see it called:

- Hotel tax or hotel occupancy tax

- Transient occupancy tax (TOT)

- Lodging tax or lodger’s tax

- Bed tax

- Room tax

These terms all describe the same fundamental concept, though the specific rules attached to each vary. For a detailed breakdown, see this explanation of transient occupancy tax and what it means for hosts specifically.

In practice, occupancy tax applies to short-term stays, which most jurisdictions define as rentals of fewer than 30 consecutive days. If a guest stays for 32 days, the rental may fall outside the taxable window entirely in some states. The taxable event is typically triggered the moment a guest pays to occupy your property for a qualifying period.

Who collects it? The answer depends on your market and your setup. In some cases, the listing platform remits the tax directly. In others, you collect it from guests yourself. In many situations, the responsibility is split. Property managers working across multiple properties often carry direct remittance duties regardless of what any platform does on their behalf.

Now that you know what occupancy tax is and who must collect it, let’s explore how tax rates and requirements vary by location.

State and local variations in occupancy tax rates and rules

How does occupancy tax work in practice? It depends heavily on where your property is located. Rates, taxable stay definitions, and filing deadlines all vary markedly between states, and often between cities within the same state.

Here is a comparison of three illustrative states to show how different the rules can be:

| State | State tax rate | Taxable stay definition | Filing deadline |

|---|---|---|---|

| Texas | 6% state rate | Short-term lodging | Varies by local rule |

| Illinois | Varies by municipality | Less than 30 days | Per filing schedule |

| Delaware | 4.5% statewide | Short-term rental | 15th of the following month |

Texas charges a 6% state hotel tax with additional local taxes layered on top, meaning a property in Houston may face a combined rate that exceeds the state base. Illinois defines taxable stays as less than 30 days and requires hosts to file specific forms, including Forms RHM-1 and RHM-7, to report and remit their obligations. Delaware imposes a 4.5% statewide short-term rental tax, due by the 15th of the following month, with additional municipal taxes possible depending on the city.

Beyond rates, occupancy tax regulations differ in several other important ways:

- Local surcharges: Cities and counties often add their own tax on top of the state rate, which means the combined rate in a popular tourist destination can be significantly higher than the headline state figure.

- Minimum stay thresholds: Some jurisdictions tax all rentals, while others only apply the tax to stays below a certain number of days.

- Exemption rules: Long-term tenants, government travelers, or guests staying beyond a set number of nights may qualify for a full or partial exemption.

- Filing frequencies: Monthly, quarterly, and annual filing schedules all exist depending on the jurisdiction and your revenue level.

Pro Tip: Check both your state tax authority and your county or city government separately. A state-level exemption does not automatically apply at the local level, and local rates can sometimes exceed state rates in high-tourism areas.

For a full overview of your obligations across different jurisdictions, the short-term rental tax obligations guide covers the 2026 landscape in detail.

Next, we’ll look at important distinctions between occupancy tax and other taxes hosts might encounter.

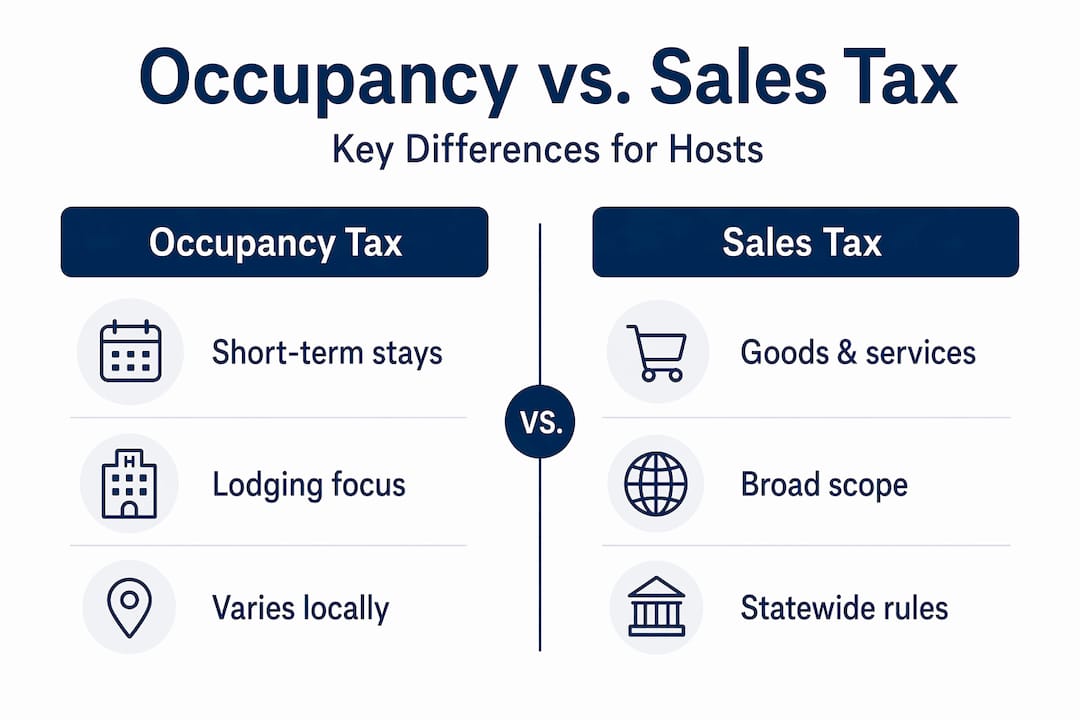

Understanding occupancy tax versus sales and other taxes

One of the most common points of confusion for hosts is the difference between occupancy tax and sales tax. They are not the same thing, and in many jurisdictions you may be required to collect both.

Occupancy tax is specifically levied on the privilege of renting lodging. Sales tax, by contrast, applies to tangible goods or certain services, and may cover items like cleaning fees, linen rentals, or other charges added to a booking. In New York, for example, a guest’s rental can trigger both state and local sales tax on top of applicable occupancy-related levies, and the taxable base for each may be calculated differently.

Key distinctions to keep in mind:

- Occupancy tax is based on the lodging charge itself, typically the nightly rate multiplied by the number of nights.

- Sales tax may apply to additional charges such as cleaning fees, pet fees, or optional add-ons depending on state rules.

- Permanent resident exemptions: Some states stop applying occupancy tax once a guest has stayed long enough to be classified as a permanent resident, often after 30 or 90 consecutive days.

- Multiple filings: You may need to submit separate returns for occupancy tax and sales tax to different agencies, even for the same rental period.

Hosts managing multiple properties face compounded complexity because layered tax requirements differ across jurisdictions, and mixing up which tax applies to which charge can result in under-collection or over-collection. Both create problems. For additional guidance on the full tax picture, visit this resource on vacation rental taxes.

Pro Tip: If you charge a cleaning fee separately from your nightly rate, check whether your state includes cleaning fees in the occupancy tax base or the sales tax base. In many states, it is one or the other, but in some it is both.

With these distinctions in mind, let’s explore operational challenges, especially when using third-party platforms for rentals.

Occupancy tax collection and reporting with third-party platforms

Many hosts operate under the reasonable belief that if their listing platform collects the tax, their compliance obligation is complete. This is incorrect in a significant number of jurisdictions.

Even when platforms collect occupancy tax, hosts often must file returns reporting the taxes collected on their behalf. In Clinton County, New York, for example, this requirement exists regardless of whether the platform has already remitted the funds. The filing requirement and the remittance requirement are treated as separate obligations.

Here is how to approach tax reporting when you use a listing platform:

- Confirm your platform’s coverage. Review your platform’s tax collection and remittance page for each jurisdiction where your property is located. Coverage varies by city and state, and a platform may collect in one market but not another.

- Register with your local tax authority. Even if your platform remits on your behalf, many jurisdictions require you to hold a tax registration number and file returns independently.

- Reconcile your records regularly. Compare platform payouts against expected tax amounts collected each month. Discrepancies between what the platform reports and what your local authority expects can trigger audits.

- Retain documentation. Keep records of every booking, the amount collected, and any platform tax remittance statements. These are your defense in an audit.

What happens when hosts skip these steps? The consequences include back taxes owed, interest charges, and fines that can significantly exceed the original tax liability. To understand the full scope of risk, see this breakdown of Airbnb host penalties and what triggers them.

- Direct booking arrangements are a particularly high-risk area. If you accept bookings through your own website or by phone, you carry the full collection and remittance burden yourself with no platform involvement at all.

- Property managers who bill guests directly rather than through a platform take on the collection responsibility entirely, and must account for this across every property in their portfolio.

Beyond collection and reporting, compliance also involves licensing and registration, which we will cover next.

Licensing, registration, and practical compliance steps for hosts

Collecting and remitting occupancy tax is only part of the legal requirement. Before you collect a dollar, you typically need to be registered with the relevant tax authority. In many markets, is occupancy tax mandatory to register for? Yes. Registration is often a legal prerequisite for operating at all.

Operational compliance generally requires registration with taxing authorities and sometimes both a general business license and a specific lodging or lodger’s tax license. Denver, for example, requires short-term rental hosts to hold a short-term rental license in addition to registering for lodger’s tax separately. Missing one of these registrations can result in operating without authorization even if you have the other.

A practical compliance checklist for hosts includes:

- Register with your state tax authority for occupancy or lodging tax before your first booking.

- Register with your local authority separately, as city and county requirements are often independent from state requirements.

- Obtain any required business licenses for operating a short-term rental in your jurisdiction.

- Set your minimum stay in accordance with local tax threshold rules if a particular stay length triggers or avoids the tax.

- Maintain detailed booking records including guest names, stay dates, gross rental income, and taxes collected per reservation.

- Calendar your filing deadlines for every jurisdiction where you operate. Missing a deadline is a compliance failure even when you owe nothing.

Pro Tip: If you manage properties in multiple cities or states, build a compliance calendar at the start of each year that maps out every filing deadline for every jurisdiction. What is due monthly in one city may be due quarterly in another.

For more on the registration side of compliance, the guide on rental registration for hosts provides jurisdiction-specific context worth reviewing.

Why occupancy tax compliance is more complex than most hosts realize

Here is something most compliance guides will not tell you directly: the complexity of occupancy tax does not come from any single rule being difficult to follow. It comes from the sheer number of independent rules that apply simultaneously, and from the expectation that you, as the host, know all of them without being told.

Most hosts discover a gap in their compliance not through proactive research but through an audit notice or a platform notification. By then, liability has already accumulated. The challenge with short-term rental compliance is that the burden of knowledge rests entirely on the operator, and local rules change without any automatic notification to the people they affect.

Third-party platforms have made this worse in a specific way. When a platform handles tax collection for some jurisdictions but not others, it creates a false sense of security. Hosts see taxes being deducted from payouts and assume everything is handled. They do not check whether they still need to file a return, whether local taxes are covered, or whether a new city-level tax has been added since they first set up their listing.

The administrative work required is also genuinely significant. Distinguishing occupancy tax from sales tax, tracking exemptions, reconciling platform statements, filing separate returns for multiple jurisdictions, renewing registrations on different schedules. These are not tasks that resolve themselves. They require consistent, documented effort. The hosts who face the fewest problems are the ones who treat compliance as an ongoing process rather than a one-time setup task.

Simplify occupancy tax compliance with STR Comply

Occupancy tax compliance is not static. Rules change, new taxes are added, and platforms update their remittance coverage without always notifying hosts. Staying current across multiple markets while managing bookings and guests is a genuine operational challenge.

STR Comply gives short-term rental hosts and property managers the tools to stay ahead of local occupancy tax requirements without spending hours researching every jurisdiction manually. The platform screens local tax obligations automatically, consolidates filing deadlines, and provides real-time guidance on what your platform does and does not handle on your behalf. Use the STR Comply tax report tool to instantly check your property’s specific tax obligations, permit requirements, and compliance status by location. For hosts managing multiple properties, it replaces the guesswork with documented, current information so you can operate with confidence rather than liability exposure.

Frequently asked questions

What types of short-term rentals are subject to occupancy tax?

Short-term rentals where guests stay less than the local taxable threshold, often under 30 days, are typically subject to occupancy tax, including houses, apartments, and condos rented through platforms or directly. Illinois defines taxable stays as less than 30 days for hotel operators, which applies equally to short-term rental hosts.

Who is responsible for collecting occupancy tax when using platforms like Airbnb?

While some platforms collect and remit occupancy tax on your behalf, many jurisdictions require hosts to file returns reporting taxes collected, so you should verify local rules and maintain accurate records. Hosts often must file tax returns even when third parties collect and remit occupancy tax.

How often do I need to file and remit occupancy tax payments?

Filing frequencies vary by location, monthly, quarterly, or annually, so check your local taxing authority’s rules to meet specific deadlines and avoid penalties. Delaware requires monthly filing by the 15th of the following month for its short-term rental tax.

Is occupancy tax the same as sales tax on my rental?

No, occupancy tax is separate and specifically targets lodging rental privileges, while sales tax may apply to tangible goods or services added to the booking, and you may need to collect both. Occupancy tax differs in base and scope from sales tax across most jurisdictions.

Recommended

Check your city's STR regulations

Free compliance reports for 100+ US cities. Permits, taxes, zoning — all in one place.

Check My Address — Free